- Europe needs to step up. A barbell strategy could be the best way to play it.

- GBP chart is really interesting, what if it contains a larger macro message.

- Single digit oil, inflation is tomorrows problem, it isn't todays.

- Fed is threading the needle to control USD, but it can't answer the demand side.

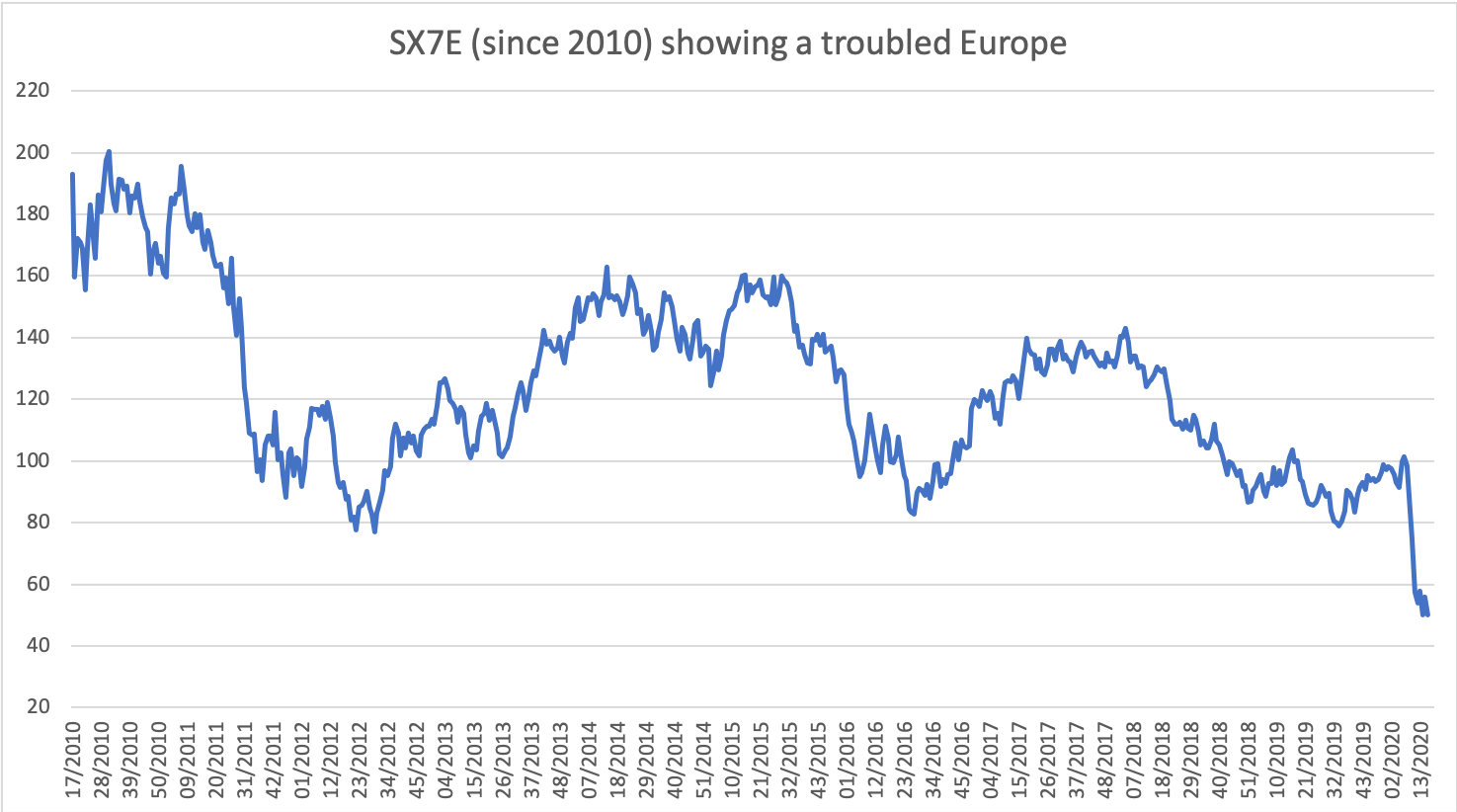

Europe needs to step up, a barbell strategy for EUR

"Whats at stake is the survival of the European project" - Emmanuel Macron

Without being too alarmist, it appears the EMU is at a key point in its history, and its response to date is insufficient, especially as it relates to its southern members. Europe has hit a fork in the road, provide a safe asset that at the same time assists the southern countries which conveys some sort of symmetry and commitment to the project, or don't, and face the political consequences.

The most recent meetings of European finance ministers was a chance for the northern European countries to really prove to the periphery that the project is worth it. One of the key things the north has to prove to the south, especially in a political context, is the idea symmetry. In terms of perception, the "transfer" has been, the north takes your productivity, and in return you get the north's borrowing rates. So when times are good, Italian productivity is turned into higher German property prices. However, it can be evened out that when an exogenous shock comes, one so big that is existential, the north says, you borrow where we borrow.

Unfortunately, that has not been the response to date. Instead, what the southern countries are seeing is, when times are good, the productivity transfer happens, and when things go wrong, the weakest among us go the ESM.

Europe has a chance to kill two birds with one stone, create a safe asset and prove the merits of the project to its most skeptical members. So far, they have dropped the ball.

The question is, is the ESM and joint issuance interchangeable, the answer as we know is no. Two key issues even if unconditionally has been agreed. First, stigma, and second, Italy has shoulder this debt load. So let's look a few years into the future, say 2022. Things have calmed down, the economy is back at operating around potential. Every six months, the Commission will give the Italians a hard time about their debt being +150% of GDP.

Eurobonds v ESM, comes down to a simple breakdown, even if technicals appear similar with unconditionality added. The point is a perception of political solidarity. Even with the disparity of unconditionality, the negative legacy still resonates and has the perception of treating them as second rate citizens. Europe will miss the forest for the trees if their message is that there is negligible difference between ESM unconditionally and a common issuance scheme.

The bottom line is, Italy thinks Europe was slow to respond to the health crisis when they needed help, which the president of the Commission has since apologized for, and now they are going to be perceived as not helping in a financial sense by forcing them to use the ESM. It is hard to see how there are not significant political consequences to this, especially as the voices who can convey this, already are on the Italian political scene and have a pretty powerful voice. According to domestic polls in Italy, confidence in European institutions has gone down in a month from 42% to 27%.

Europe can still save itself

One of the things that makes Europe so interesting right now is, the flip side of this, if it were to take place, is immensely bullish the EMU and the single currency. With one stone, Europe can solidify its project by extending an olive branch to the south and be a recipient of massive flows from reserve managers and a global savings pool that is desperate for cash like alternatives. The introduction of a safe asset in this environment would be met with massive demand, even from people outside the reserve manager community. Japan for example, is a massive buyer of OATs because the combination of PSPP and a lack of German/Dutch issuance have left OATs by themselves for reserve managers and Asian pensions.

It doesn't even necessarily have to be coronabonds. Vitor Constancio in a recent blog post put forth something interesting. He postulates that the Commission could issue debt under the context of Treaty Article 122.2 which states "Where a Member State is in difficulties or is seriously threatened with sever difficulties caused by natural disasters or exception occurrences beyond its control, the Council, on a proposal from the Commission, may grant under certain conditions, Union financial assistance to the Member state concerned." Either way, the point is, there are technical ways for Europe to have its cake and eat it too. Which is, northern countries not having to joint issue and southern countries would avoid the stigma and get relief. While the situation may be binary, the solutions are not.

If Europe were to invest itself, with the commensurate response this crisis requires, it could solidify the monetary union and encourage foreign flow from reserve managers and global savings. Hard to see how that wouldn't be immensely bullish EUR.

This duality is what sets up a barbell type strategy for Europe. Either they get it right, or they continue down this current path that surely leads to negative political consequences. Do joint issuance, save the EMU from political backlash and introduce a safe asset in time of tremendous demand for cash alternatives. Or, the market prices some nasty tails from the political backlash, which even Draghi in May 2018 struggled to deal with.

GBP in a world of fiscal/monetary mix, the post Osborne/Carney UK

One of the more interesting charts to me in global macro right now is a broad reading of GBP using effective exchange rates. Since Brexit it has been making a long basing formation.

Typically, in a crisis, GBP comes under pressure as it runs a large external account deficits with high external debt levels. However, despite its initial reaction in darker days of March, GBP has been resilient, even relatively strong. This comes with a very aggressive monetary/fiscal easing that has included a temporary reactivation of a scheme that makes it possible for the BoE to finance public spending directly. So the UK has gone into this shock with an overhang of political clouds from the transition talks with the EU, weak external account (c/a, NIIP, external debt) and has done the most aggressive version of monetization, and with all of that GBP/Gilts keep rallying......

It's absolutely possible that GBP is pricing spillovers from funding markets, and there is no massive GBP breakout coming. With that aside, there could be a broader macro point in GBP that is worth considering. It is possible that GBP is pricing, this aggressive policy mix, as "the right thing." I.e. what if this is the UK's 1931 and breaking the gold standard, which led to a few a years of higher TFP and higher real growth. There is no FX deval this time, but UK policy is being "set free" after years of fiscal austerity and defensive supply side based monetary policy making.

One of the more interesting charts to me in global macro right now is a broad reading of GBP using effective exchange rates. Since Brexit it has been making a long basing formation.

Typically, in a crisis, GBP comes under pressure as it runs a large external account deficits with high external debt levels. However, despite its initial reaction in darker days of March, GBP has been resilient, even relatively strong. This comes with a very aggressive monetary/fiscal easing that has included a temporary reactivation of a scheme that makes it possible for the BoE to finance public spending directly. So the UK has gone into this shock with an overhang of political clouds from the transition talks with the EU, weak external account (c/a, NIIP, external debt) and has done the most aggressive version of monetization, and with all of that GBP/Gilts keep rallying......

It's absolutely possible that GBP is pricing spillovers from funding markets, and there is no massive GBP breakout coming. With that aside, there could be a broader macro point in GBP that is worth considering. It is possible that GBP is pricing, this aggressive policy mix, as "the right thing." I.e. what if this is the UK's 1931 and breaking the gold standard, which led to a few a years of higher TFP and higher real growth. There is no FX deval this time, but UK policy is being "set free" after years of fiscal austerity and defensive supply side based monetary policy making.

What did every MPC inflation report say once the bank started hiking rates. "MPCs central projection, therefore, a small margin of excess demand emerges by late 2019 and builds thereafter, feeding through into higher growth in domestic costs than has been seen in recent years." The perception of reduced economic potential from Brexit led the BoE to a tighter posture than it needed to be.

The UK has lost its Osborne/Carney combination of tight fiscal and hawkish monetary based on a shrinking supply side and has replaced it with an aggressive monetary/fiscal mix. The currency is usually not the outlet to represent such a transition (and maybe it's a poor way to play it), but it could be this time around as this transition seems very bullish, especially v the obvious constraints that Euro countries are facing. A currency is an outlet for economic imbalance. Aggressively trying put an economy back together in the name of preventing further deviations from potential, is not an imbalance, even if the numbers seem big. What if GBP is saying the UK economic response is right......

Short EURGBP seems compelling. UK policymaking have been set free, Europe is still constrained. 90c looks like a decent top and should serve as a good stop.

Oil is going to single digits, inflation is tomorrow's problem

The Saudis and Russian both knew there was no rebalancing the market into this sort of demand shock, and decided it was time put shale in the grave, and they are doing just that. Global demand is off somewhere between 20-30mbd, Cushing is likely to be close to filled up by the middle of May (inventories are rising at +16mbd per week), and rolling shut ins in the US/Canada will begin to take place.

This dynamic has set up the super contango in the oil futures curve, and with few bullets left from geopolitical forces, oil is still a compelling short. One, there is plenty of room for oil prices to continue to fall before shut ins really accelerate and once storage gets overwhelmed that is when you get negative prices in regional contracts as basis continues to be super wide. And because of this current storage dynamic, the market is paying you an absurd amount of carry to be short. The May roll has been absolutely hideous, but it seems like nearbys will continue to trade in steep contango with the just an absolutely vicious rolldown. So oil has no demand, storage is filling up and you basically need to make 20% just to beat the roll, how can anyone be long this thing and yet inflows into USO ETF continue and that is likely the only thing keeping up the June contract. These USO inflows are about to get killed. And they are the only reason the active June contract is still above 20 bucks.

So what are the consequences of single digit oil in a global macro sense. The first thing that comes to mind is the inflation question. I'm sympathetic to the inflationary endgame; disruptions from supply chain regionalization, public policy more focused people with higher MPCs. It is all very plausible, but it will take time.

Supply chains will face political pressure and a reevaluation of the trade off between the wage arbitrage and transportation logistics. But these things take time unless politics hastens the adjustment, which could very well happen.

However, the path to supply chain regionalization and more targeted public policy is with massive labor market slack, an oil price that is single digits and an increased propensity towards savings as covid19 leaves its economic PTSD. Despite massive public sector deficits, it is very hard to see how a massive imbalance between supply and demand in the aggregate will form in this backdrop, even if the supply chain disruptions are worse than many are projecting.

The trading consequences of $10 oil, a few things:

- Breakevens have gone too far. Stocks are not pricing some miracle recovery, as Mike Green in recent post said, the stock market more so represent transactions than information, and the combination of passive and massive foreign savings demand along with a liquidity bazooka all are colluding to raise asset valuations, even into uncertainty. Real yields will likely begin to rise again.

So far these two seem pretty correlated. That could continue, but may not make sense to read too much into the message. The economic imbalance is there is too much private capital going after too few investments, not that there is too much govt spending into too little economic supply.

- USDCAD could go to 1.50. Combination of an oil price in low single digits or even negative (WCS), and what will be a private sector balance sheet deleveraging should put a cap on how far an economic recovery will go. Also the BoC has been pretty aggressive themselves with cutting all the way down to its effective lower bound (0.25%) and doing three pretty big liquidity programs (BA purchase facility, Provincial Money Market Purchase Program, CP purchase program). That is all before they said at last weeks MPR meeting that they will take down 40% of each new gov't treasury bill auctions, and said they're program of purchasing gov't bonds (min 5b a week) could be increased any time. Canada went into this crisis with an economy near potential, as the BoC likes to point out, but it also went into with relatively high levels of household and private sector debt. The combination of a slower private sector response and very low oil prices all with an aggressive central bank could make CAD pretty vulnerable.

Controlling USD is like threading a needle, what about the demand side?

The market seems torn between two camps as it relates to USD, and it is quite binary. This is quite interesting as it seems like a very nuanced dynamic. And again, the demand side is likely being underestimated with not that many alternatives for capital to go.

However, the path to supply chain regionalization and more targeted public policy is with massive labor market slack, an oil price that is single digits and an increased propensity towards savings as covid19 leaves its economic PTSD. Despite massive public sector deficits, it is very hard to see how a massive imbalance between supply and demand in the aggregate will form in this backdrop, even if the supply chain disruptions are worse than many are projecting.

The trading consequences of $10 oil, a few things:

- Breakevens have gone too far. Stocks are not pricing some miracle recovery, as Mike Green in recent post said, the stock market more so represent transactions than information, and the combination of passive and massive foreign savings demand along with a liquidity bazooka all are colluding to raise asset valuations, even into uncertainty. Real yields will likely begin to rise again.

So far these two seem pretty correlated. That could continue, but may not make sense to read too much into the message. The economic imbalance is there is too much private capital going after too few investments, not that there is too much govt spending into too little economic supply.

- USDCAD could go to 1.50. Combination of an oil price in low single digits or even negative (WCS), and what will be a private sector balance sheet deleveraging should put a cap on how far an economic recovery will go. Also the BoC has been pretty aggressive themselves with cutting all the way down to its effective lower bound (0.25%) and doing three pretty big liquidity programs (BA purchase facility, Provincial Money Market Purchase Program, CP purchase program). That is all before they said at last weeks MPR meeting that they will take down 40% of each new gov't treasury bill auctions, and said they're program of purchasing gov't bonds (min 5b a week) could be increased any time. Canada went into this crisis with an economy near potential, as the BoC likes to point out, but it also went into with relatively high levels of household and private sector debt. The combination of a slower private sector response and very low oil prices all with an aggressive central bank could make CAD pretty vulnerable.

Controlling USD is like threading a needle, what about the demand side?

The market seems torn between two camps as it relates to USD, and it is quite binary. This is quite interesting as it seems like a very nuanced dynamic. And again, the demand side is likely being underestimated with not that many alternatives for capital to go.

A few dynamics:

If the battle for global savings is US risk assets v EM/Europe or China, US will likely win.

- Balance sheet constraints were a key reason for USD strength in the onset of the crisis as many Asian non bank financials use that balance sheet to hedge/fund USD credit risk. With the Fed flooding the market, local CBs more focused on reaching end users, its hard to see what really aggravates the FX swap market as cross currency basis will trade with a much less negative bias. The effect of UST bill issuance will probably be key in monitoring this. But as a whole, the Fed is getting USD to those who need it, and that could really serve as a cap on USD strength as it has so far. Especially if Zoltan is right and the Fed caps bill yields.

- So Asian savings has to worry less about funding/hedging duration trades, and the Fed is implicitly backstopping many of the instruments they are long, investment grade credit. That means the US is still a relatively attractive place for global savings, especially if this duality of a tame FX swap market, curvature which reduces hedging cost and a Fed determined to protect high quality risk assets, seems like USD is still a decent home for global savings.

- One of the key spillovers of QE is meant to be the portfolio balance channel. However this channel becomes a bit more confusing when everyone is doing it, i.e. no global carry trade. Is real money going to fund EM, seems unlikely, they have no growth and no carry.

Makes sense for US tech to continue to attract capital over Emerging markets. This trade plays on two themes:

1) DM has balance sheet to absorb this mess, EMs do not.

2) In a world of no carry, capital will prefer US given growing asset class in an appreciating currency.

- EM crisis response seems to be correct, but it will require a continued adjustment in the exchange rate. Even, if IMF liquidity facility and an SDR allocation were to come in a meaningful way, that will only give local CBs more room to continue cut rates. If the response remains underwhelming, then places like (ZAR/IDR/MXN) will continue to go through the "original sin redux" as Carstens and Shin have noted. That is the problem with having such a high percentage of your local ccy bond market being owned by foreigners. And, the cut rates/let fx go, doesn't actually incentivize a buildup of domestic savings.....

- Balance sheet constraints were a key reason for USD strength in the onset of the crisis as many Asian non bank financials use that balance sheet to hedge/fund USD credit risk. With the Fed flooding the market, local CBs more focused on reaching end users, its hard to see what really aggravates the FX swap market as cross currency basis will trade with a much less negative bias. The effect of UST bill issuance will probably be key in monitoring this. But as a whole, the Fed is getting USD to those who need it, and that could really serve as a cap on USD strength as it has so far. Especially if Zoltan is right and the Fed caps bill yields.

- So Asian savings has to worry less about funding/hedging duration trades, and the Fed is implicitly backstopping many of the instruments they are long, investment grade credit. That means the US is still a relatively attractive place for global savings, especially if this duality of a tame FX swap market, curvature which reduces hedging cost and a Fed determined to protect high quality risk assets, seems like USD is still a decent home for global savings.

- One of the key spillovers of QE is meant to be the portfolio balance channel. However this channel becomes a bit more confusing when everyone is doing it, i.e. no global carry trade. Is real money going to fund EM, seems unlikely, they have no growth and no carry.

Makes sense for US tech to continue to attract capital over Emerging markets. This trade plays on two themes:

1) DM has balance sheet to absorb this mess, EMs do not.

2) In a world of no carry, capital will prefer US given growing asset class in an appreciating currency.

- EM crisis response seems to be correct, but it will require a continued adjustment in the exchange rate. Even, if IMF liquidity facility and an SDR allocation were to come in a meaningful way, that will only give local CBs more room to continue cut rates. If the response remains underwhelming, then places like (ZAR/IDR/MXN) will continue to go through the "original sin redux" as Carstens and Shin have noted. That is the problem with having such a high percentage of your local ccy bond market being owned by foreigners. And, the cut rates/let fx go, doesn't actually incentivize a buildup of domestic savings.....

- So while oil and shutdowns will keep current account balances relatively in tact, as we have seen in places like the Philippines where the Luzon shut down has cut import demand to zero. This gives the BSP plenty of room to get dovish. However, what happens when it opens up, and remittances drop, PHP wont be as strong as it is now with the policy rate at 2.75%. The point is, as unfortunate as it is, this EM adjustment in the exchange rate will likely be structural and the bias will continue to be for USD/EM to trade higher.

No growth/no carry, this could be more structural.

- And as a last one in terms of where capital could go, as we said above, Europe is vulnerable.

Overall: yes, the Fed has done a lot to clean the global USD funding pipes, but it's hard for them to fight the fact that the US is still the preferred destination for foreign capital. And that at the end of the day will likely be the balancing act of USD going forward. My bias is that it goes higher, but the Fed could have established a pretty decent cap by dislodging the USD funding market through these massive liquidity injections.

One point that I think is overrated as a reason for pending USD weakness is the "twin deficit." This likely underestimates how much bigger deficits can get before they worry USD. Ito & McCauley from the BIS showed us that global imbalances look a lot different when key currencies are the unit of analysis and not GDP.

The world likely still lives in a USD smile world. Until a demand impulse from RoW is to emerge, the market will continue to focus on the risk on/off dynamic of how USD can benefit in either, higher risk assets or a flight to safety. I think a key answer in the USD, risk assets etc, will be found in global term premia. Either it rips in response to the massive size of this global easing impulse, or it lags and continues to favor the imperial circle, strong USD and elevated US asset prices.

Thanks for reading, stay safe, best way to be in touch is email, jonturek@gmail.com

No growth/no carry, this could be more structural.

- And as a last one in terms of where capital could go, as we said above, Europe is vulnerable.

Overall: yes, the Fed has done a lot to clean the global USD funding pipes, but it's hard for them to fight the fact that the US is still the preferred destination for foreign capital. And that at the end of the day will likely be the balancing act of USD going forward. My bias is that it goes higher, but the Fed could have established a pretty decent cap by dislodging the USD funding market through these massive liquidity injections.

One point that I think is overrated as a reason for pending USD weakness is the "twin deficit." This likely underestimates how much bigger deficits can get before they worry USD. Ito & McCauley from the BIS showed us that global imbalances look a lot different when key currencies are the unit of analysis and not GDP.

The world likely still lives in a USD smile world. Until a demand impulse from RoW is to emerge, the market will continue to focus on the risk on/off dynamic of how USD can benefit in either, higher risk assets or a flight to safety. I think a key answer in the USD, risk assets etc, will be found in global term premia. Either it rips in response to the massive size of this global easing impulse, or it lags and continues to favor the imperial circle, strong USD and elevated US asset prices.

Thanks for reading, stay safe, best way to be in touch is email, jonturek@gmail.com

Thanks for this amazing article on Cheap Convexity was Just searching for Moving Companies and found this amazing website of yours.

ReplyDelete