1) Q2/Q3 2021 is setting up to be a clash between the Fed's new reaction function and upside risks. The Fed will likely lean into "opportunistic reflation."

2) 2010-2020 was a bull market in risk premium, what if covid and the massive policy response since was a turning point in distributional terms?

The Fed wants to lean into "opportunistic reflation."

The Fed finds itself at an interesting juncture. The backdrop is pretty simple, the very near term is highly uncertain while the medium term looks far more robust than the September dots show. The problem is, FCIs are about as loose as they've ever been, so while things like WAM extensions have been thrown around, they don't really accomplish much. So the Fed will likely stay put, as Clarida said at Brookings, policy is in a good place.

With all that said, this will likely not be the focus of the market outside of some on the day knee jerk reactions. The real Fed message the market needs to see is that AIT means business. The Fed going forward will be much more about adding barriers to any form of tightening as opposed to looking for new ways to ease.

As has been discussed in many market and academic circles, the middle of next year is setting up as a "cage match" between the Fed's new reaction function and the upside risk of a faster than expected cyclical normalization. So the question for the market right now is, with rates hugging key technical levels and the belly beginning to cheapen on a relative basis, what if the Fed blinks?

In 2019 the Fed threw the Phillips Curve orthodoxy out the window and was cutting rates into an economy that had an u3 rate decently below most estimates of NAIRU. The post DSGE era arrived pre covid. Realized outcomes matter more than expected ones when it comes to upside risks. And if the market thinks the Fed will be startled by a comps based rise in inflation during the middle of next year, Brainard was already hoping for things like that to materialize, even pre covid. The Fed wants to lean into the upside scenario.

"the Committee would make clear in advance that it would accommodate rather than offset modest upward pressures to inflation in what could be described as a process of opportunistic reflation."

"Stabilization to accommodation"

One of the key themes that we have learned from Brainard this year is how she is thinking about the reaction function in light of the shock and policy constraints at the lower bound. Something she highlighted in a September speech is that policy should begin to transition from "stabilization to accommodation." This may have been the most descriptive three words explaining the Fed's reaction function going forward. The Fed sees itself as a line of defense, or a buyer/lender of last resort in a shock. And in a recovery it sees itself as an exponent allowing the recovery itself to cyclically expand the easing posture of policy. Thus "accommodating" a recovery via accelerating it. Which is something we have already seen through this divide between breakevens and real yields.

At the ZLB, the balance sheet stabilizes, forward guidance accommodates.

In terms of thinking about how the Fed will navigate this cyclical transition, the Fed will be much more worried about the destination and not the location. Which is to say, policy will be judged by where the economy is relative to the Fed's longer run goals, not where the economy is relative to the size of policy accommodation.

"As we move to the next phase of monetary policy, we will be guided not only by exigencies of the covid crisis, but also by our evolving understanding of the key longer-run features of the economy, so as to avoid the premature withdrawal of necessary support." - Brainard July.

Fed guidance has to evolve to continue enforcing it

The question now is, how does the Fed enforce this, as the bond market is clearly itching to play catchup to these massive moves in cyclicals across asset markets. This is likely where forward guidance has to go into overdrive to make sure the Fed can continue this powerful duality of real yields lower, breakevens higher. And because many CBs are currently/have already put into place similar sorts of guidance, the Fed will have plenty of academic and real world policy work to lean on.

In terms of reinforcing the CBs reaction function and making sure that the recovery is not affected by any sort of financial market tightening, the Fed will likely have to be more clear about balance sheet guidance as that is so key in a policy sequencing sense. Benoit Coeure spelled it out in 2018.

"asset purchases are necessary at the lower bound to reinforce forward guidance."

"we have also seen that, as the outlook improves, the signal that asset purchases send regarding the likely date of a first rate hike becomes increasingly important for anchoring the medium to long-term segment of the curve."

The Fed wants to communicate to markets that despite the positive developments regarding the vaccine and the potential for upside risks in 2021, policy will not budge until the goals explained in the updated MPF (monetary policy framework) are met. QE is a big part of that policy calibration.

In March of 2016, Peter Praet of the ECB also explained the key policy linkages between BSP and interest rates, especially at the effective lower bound. At the time, the ECB had adjusted the forward guidance on the key ECB interest rates to imply a "sequencing" between rate policy and APP.

"The APP enhanced the effectiveness of our forward guidance on policy rates via the signalling channel, underscoring our commitment to keep rates low for as long as necessary to achieve the stated objective of our policy."

This sounds awfully similar to what Brainard was saying in February with regard to interest rate caps, well QE can act as de facto rate caps.

"To strengthen the credibility of the forward guidance, interest rate caps could be implemented in tandem as a commitment mechanism."

So what does this all look like?

Whether the Fed statement looks more like the BoC, "Bank will continue QE until recovery is well underway" or even more aggressive and ECB like by linking QE to the policy rate, the Fed will look to link BSP to longer run goals and not see it as an emergency tool. So while many on the street are looking for the Fed to respond to an upside risk scenario, the Fed will likely lean into it. For that to fully happen, preventing a taper tantrum is key and having balance sheet guidance is the best way to prevent one. The Fed can use BSP to reinforce its forward guidance stance and have it serve as a form of commitment mechanism which Brainard talked about. In market terms this means that rates will continue to be an inferior expression of positive economic outcomes. And because they are inferior, positive outcomes can have a more outsized effect on cyclical beta than they usually would have.

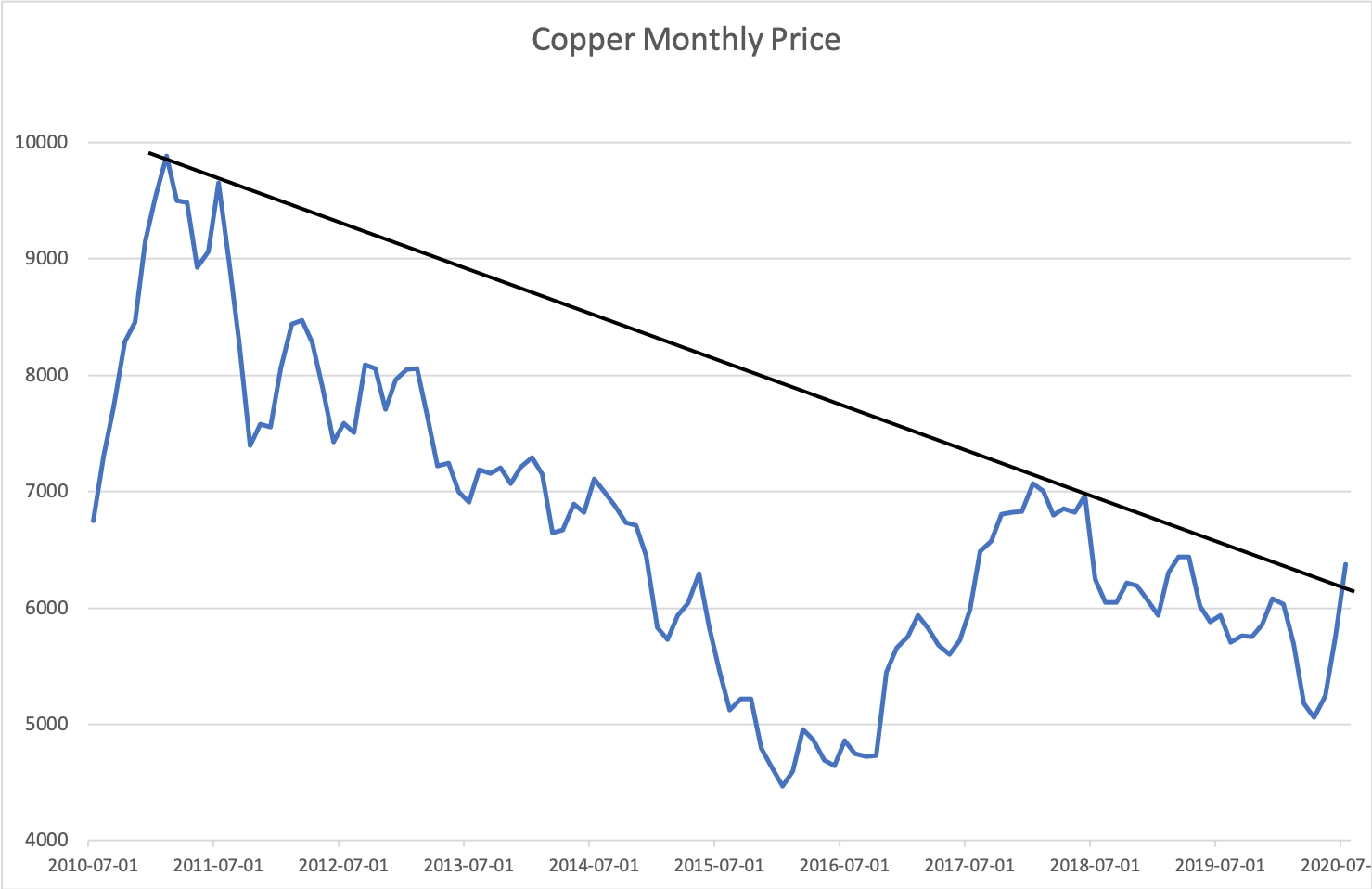

2010s were a bull market in exogenous risk

One of the defining themes of the post GFC period was this long safety short cyclicals theme. Given the low level of rates, the scarring from the GFC/Euro crisis and skew towards deflation, risk premium traded at a very elevated level. The knock on effect of this bull market in risk premium was that anything the market determined was "safe" was given an infinite valuation. The trade was capital protection, not capital appreciation, and that was in the context of an asset shortage on a global level. This sort of pricing was entirely logical. One, given the hysteresis of the GFC, and rising exogenous risk from geo-political events, the structural bias to price deflationary risk made a lot of sense. This was also in the backdrop of rising government surplus' in places like Europe and Asia, a global savings glut and a structural change in terms of Chinese growth levels which the global economy had become highly dependent on via exports.

So the macro backdrop was:

- Economic hysteresis.

- Slower levels of global trade.

- Rising exogenous risk (geo-politics).

- A rising USD.

Which is all to say, it made sense for the market to continuously price a relatively high level of risk premium, as that was certainly what the skew of potential/realized outcomes favored. And all of this culminated in the perfect economic shock, a global pandemic recession.

Risk premia has been quite elevated on a structural level

Risk premia has been quite elevated on a structural level

One of the more interesting findings in a terrific Emmanuel Farhi paper that he presented at the ECB in 2018 was, despite a much lower level in the discount rate, risk premia has been building for a while. Farhi's framing is actually a challenge to the global savings glut thesis, because the level of risk premia has risen despite the fact that MPK (marginal product of capital) has stayed fairly high. In theory, savings should drive everything lower, but the MPK rate has stayed elevated. So there has been a fairly wide wedge between the returns on private capital and risk free rates and elevated levels of risk premia likely have a lot to do with that.

Divide between "safety and "risk" has been a clear trend in markets

This sort of bifurcation between safety and cyclical beta has had a profound effect across global markets. The well known long tech short everything else trade, long USD, flatteners in the bond market etc. At their core, these trades had a lot of overlap, the market continued to ride the skew of "bad" things were just much more likely than "good" things.

If we look at FX, safety (USD, CHF) was a 10y bull market and cyclical (SEK, AUD) beta got crushed for a decade.

What if the post policy backstop world changes these distributions even slightly?

One of the more interesting questions post covid will be, does the calculus regarding risk premium change at structural level and not only at a cyclical one. I.e. the market right now is reducing the level of risk premium on the back of the vaccine results and their high level of efficacy. But the bigger question is what if the post covid global economy is able to exhale just a bit from a decade of relentlessly high levels of risk premium? It is still likely a very low delta but it is possible the skew of the last decade has changed. The reason is that despite some fumbling in terms of US fiscal or NGEU disbursements etc. the global policy focus is intensely on preventing "bad" outcomes. The question going forward is, if the left tail footprint is being structurally lowered, even just a little, that could have a profound effect on risk distributions going forward. The Covid shock brought out all of the market/economy's vulnerabilities at the same time, the fact that so many of them were contained could change the pricing distribution going forward. Will be very interesting to see.

Happy holidays and all the best in 2021.

jonturek@gmail.com

If we look at FX, safety (USD, CHF) was a 10y bull market and cyclical (SEK, AUD) beta got crushed for a decade.

What if the post policy backstop world changes these distributions even slightly?

One of the more interesting questions post covid will be, does the calculus regarding risk premium change at structural level and not only at a cyclical one. I.e. the market right now is reducing the level of risk premium on the back of the vaccine results and their high level of efficacy. But the bigger question is what if the post covid global economy is able to exhale just a bit from a decade of relentlessly high levels of risk premium? It is still likely a very low delta but it is possible the skew of the last decade has changed. The reason is that despite some fumbling in terms of US fiscal or NGEU disbursements etc. the global policy focus is intensely on preventing "bad" outcomes. The question going forward is, if the left tail footprint is being structurally lowered, even just a little, that could have a profound effect on risk distributions going forward. The Covid shock brought out all of the market/economy's vulnerabilities at the same time, the fact that so many of them were contained could change the pricing distribution going forward. Will be very interesting to see.

Happy holidays and all the best in 2021.

jonturek@gmail.com