- Jackson Hole, the Fed’s current duality.

- Can we have a “beautiful” recovery or is fiscal in trouble?

- What if we have the USDJPY question all wrong?

- Lane's EURUSD comments were no faux pas.

Overall: One of the more interesting things going into the September ECB/FOMC meetings and the updated staff macro forecasts is they both have very important questions to answer. The ECB has to answer the EURUSD question, does 1.20 really bother them? The Fed will have to show what they can do to further ease given the SEP will continue to show them coming up short of their dual mandate goals. We know what they will do (won't do) when things get better, what can they do if things get worse?

The Fed's duality

With the culmination of their strategic review, the Fed showed the interesting duality they find themselves in. On the one hand, it is clear the Fed will not be preemptively hiking rates in this new framework, something we have known since they initiated this review in 2019.

The Fed wants to allow the economy to recover and accentuate that recovery by remaining accommodative for longer than it traditionally has. That is of course dovish. And despite some missteps in the communique with regard to what exactly inflation overshoots will look like, the bigger message should not get lost, they will be allowing inflation overshoots and FAIT is the end of the “bygone” era.

However, this sets up two camps for the Fed going into the post covid recovery.

On the one hand, if this Fed backdrop is accompanied by a continued substantial fiscal response and an inevitable vaccine, it is rocket fuel for risk assets. As we saw in Brainard's July speech, the Fed's degree of monetary accommodation will expand with the recovery. That is when forward guidance is so powerful.

On the other hand, a problem the Fed has right now is especially in regard to this framework, they are fiscal dependent in terms of creating the conditions they desire in an outcome sense. By itself, despite opening up policy space with the balance sheet and forward guidance, the Fed will struggle to generate "good" economic outcomes on their own given the lower bound constraint. As Brainard effectively put it in her July speech, the Fed is very capable in preventing left tail outcomes via their balance sheet, however in terms of "accommodation" that will largely come in a pro-cyclical fashion given the lower bound constraint.

One of the things that Bernanke noted in his January AEA speech, L4L (lower for longer) policies can only do so much if neutral rates are below 2%. And this is where the Fed likely finds themselves.

“if the nominal neutral rate is much lower than 2%, then model simulations imply that new monetary tools while still providing valuable policy space can no longer fully compensate for the effects of the lower bound.”

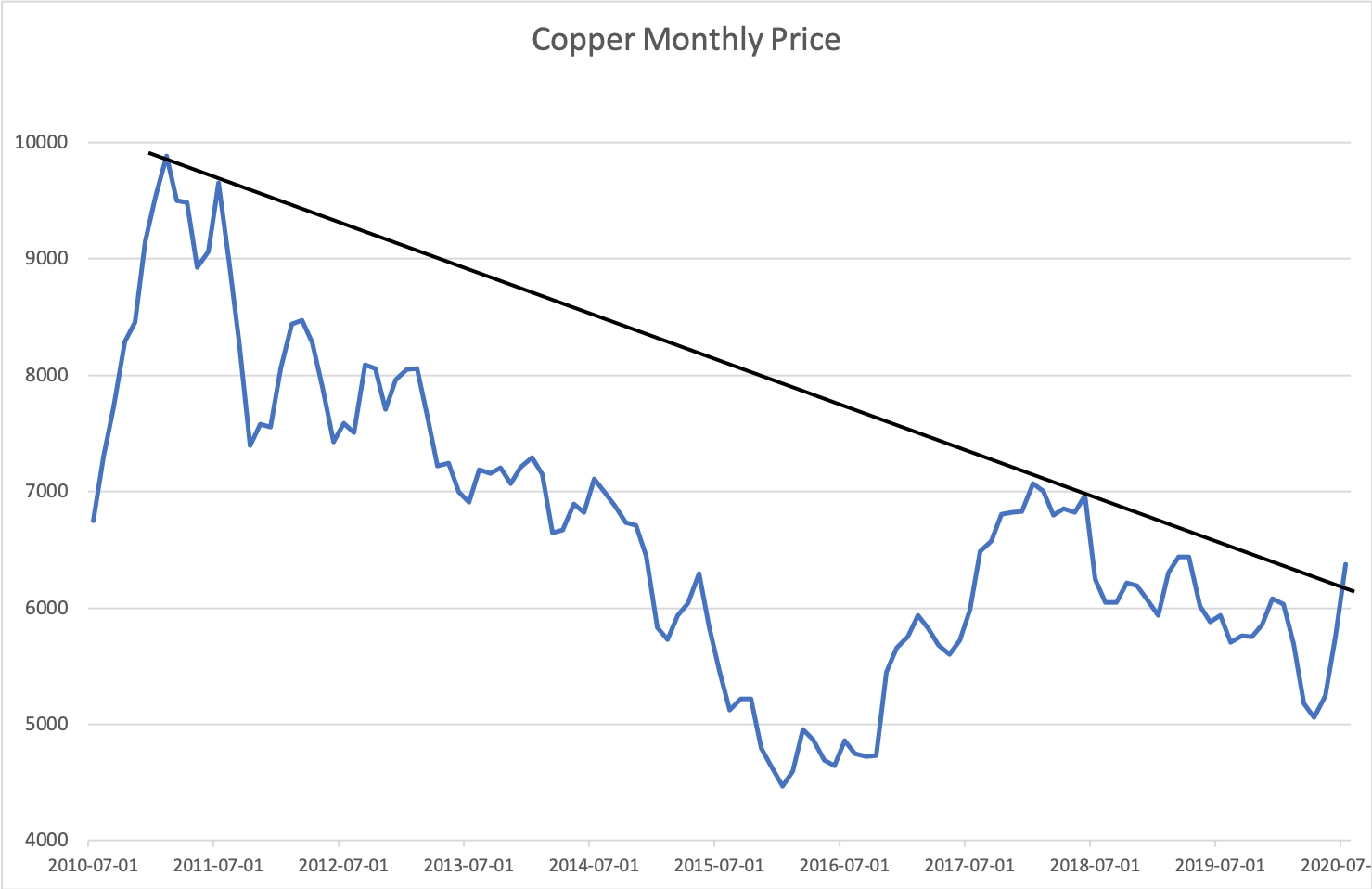

Copper may be evidence of the third camp is gaining steam

Does the market have the USDJPY question wrong?

One of the emerging questions in global macro these days is when does USDJPY breakdown and follow the broad dollar index lower. So far, USDJPY has been in a tight range due to very loose funding markets on the one hand and real money flows capping Yen strength on the other. And Yen is not going to trade on relative real rates. The question is, when does this tight range break and do we get this sort of inverse Abenomics move where USDJPY goes back to the 80s?

It's possible the market is asking the wrong question. The right question may be, what if USDJPY is able to absorb these weak dollar pressures and stay above 100, maybe even in this tight 105 range? Let’s say in a world of reflation, rising asset prices and flat term structures, Japanese policymakers are able to get what they want and effectively pin the Yen. That world is a very interesting world for Japanese stocks which are close to pressing up against multiyear resistance.

Nikkei 24k is a huge level if we get there. 3y daily chart.

This may not be actionable right now, but it is something worth watching. Of course, it is too soon to say that USDJPY won’t follow this dollar move lower and that will pose a challenge to Japanese equities, especially in a relative sense. However, given the asymmetry, it is likely worth asking the question of, let’s say we are in a durable reflation and the BoJ has figured out a way to peg JPY, that is about as constructive as it gets for Japanese equities in zero rate world. All of this is happening at close to very interesting technical levels.

Keep an eye on the ECB this week

It was a bit surprising to hear comments from Phillip Lane last week re the current level of EURUSD. It wasn’t anything drastic, and the blog posts from Schnabel have not been particularly worried re the level of the exchange rate.

“At the moment I am not worrying too much about exchange rate developments.”

However, nothing is by accident with Lane, and he wanted it out there that the EURUSD rate matters and the ECB is watching it.

This sets up two questions:

1) Lets for a second entertain the idea that +1.20 worries the ECB. This is something I am not convinced of as the ECB knows the combination of fiscal and the nature of the shock have changed the pass through dynamics. However, in this hypothetical, they care. What do they do? The street is expecting an upsized PEPP, and that makes sense. In theory, QE is two birds with one stone for the ECB, it decreases fragmentation risk and lowers the XR (exchange rate). The problem is, in practice it won’t weaken XR and I think the ECB is well aware of that. The traditional portfolio balance channel ala 2014 is broken. Upsizing PEPP has a much bigger impact on left tail pricing/accommodating fiscal than it does on the portfolio balance channel, so QE in Europe could actually be XR positive…..

Marginal QE effects have changed since Draghi started PSPP

2) Is Lagarde going to entertain rate cuts? This is something that should be off the table, and it likely won't happen because it EURUSD 1.20 is an overrated risk for EA inflation. However, it would be very interesting if Lagarde makes a nudge at getting negative term premium to go a bit further. I.e. testing that lever and see what it does to EUR. And of course, because of that most recent inflation print, she has every right to do so. The knock on if the ECB starts to push the market a bit on getting serious re DFR cuts would be huge. This would open up the same problems of 2019, where the ECB via pushing the dollar higher ends up being a duration vacuum and broadly negative risk. Also, in a more structural sense, it threatens this new world of ELB + fiscal which has been $ negative. It is a much more positive risk FX environment when the only CB really entertaining cuts is NZD and we push the policy handoff narrative. ECB entertaining cuts would threaten that so it is worth watching even if it’s a small probability. As noted above, the $ is the key outlet for a global recovery and the ECB should not want to get in the way of that.

The Fed's duality

With the culmination of their strategic review, the Fed showed the interesting duality they find themselves in. On the one hand, it is clear the Fed will not be preemptively hiking rates in this new framework, something we have known since they initiated this review in 2019.

The Fed wants to allow the economy to recover and accentuate that recovery by remaining accommodative for longer than it traditionally has. That is of course dovish. And despite some missteps in the communique with regard to what exactly inflation overshoots will look like, the bigger message should not get lost, they will be allowing inflation overshoots and FAIT is the end of the “bygone” era.

However, this sets up two camps for the Fed going into the post covid recovery.

On the one hand, if this Fed backdrop is accompanied by a continued substantial fiscal response and an inevitable vaccine, it is rocket fuel for risk assets. As we saw in Brainard's July speech, the Fed's degree of monetary accommodation will expand with the recovery. That is when forward guidance is so powerful.

On the other hand, a problem the Fed has right now is especially in regard to this framework, they are fiscal dependent in terms of creating the conditions they desire in an outcome sense. By itself, despite opening up policy space with the balance sheet and forward guidance, the Fed will struggle to generate "good" economic outcomes on their own given the lower bound constraint. As Brainard effectively put it in her July speech, the Fed is very capable in preventing left tail outcomes via their balance sheet, however in terms of "accommodation" that will largely come in a pro-cyclical fashion given the lower bound constraint.

One of the things that Bernanke noted in his January AEA speech, L4L (lower for longer) policies can only do so much if neutral rates are below 2%. And this is where the Fed likely finds themselves.

“if the nominal neutral rate is much lower than 2%, then model simulations imply that new monetary tools while still providing valuable policy space can no longer fully compensate for the effects of the lower bound.”

If neutral rates are too low, L4L can't overcome ELB by itself most of the time.

*the QE options vary by size, B being the smallest, D the biggest.

So, this is how the duality presents itself. The Fed's new framework is incredibly constructive to an economic recovery, but by itself cannot create that recovery given the lower bound constraint. And while L4L policies will help, they cannot overcome ELB by themselves as they likely could in a higher neutral rate world. The Fed will try to answer questions on their easing constraints at the September meeting. This will be an especially powerful moment as it will likely coincide with continued fiscal impasse and an SEP (staff economic projections) that shows the Fed below their dual mandate goals for the duration of the forecast horizon.

All roads lead to the Fed trying to prove themselves again in September. We know how they will act, or not act, when times get better, what will they do if things get worse…. They will have to answer that question, or at least try.

Can the Fed keep getting this chart to bull steepen?

Can we have a “beautiful” recovery?

This is a bit of a play on Mohamed El-Erian’s/Ray Dalio's “beautiful deleveraging” concept from a few years ago.

So, this is how the duality presents itself. The Fed's new framework is incredibly constructive to an economic recovery, but by itself cannot create that recovery given the lower bound constraint. And while L4L policies will help, they cannot overcome ELB by themselves as they likely could in a higher neutral rate world. The Fed will try to answer questions on their easing constraints at the September meeting. This will be an especially powerful moment as it will likely coincide with continued fiscal impasse and an SEP (staff economic projections) that shows the Fed below their dual mandate goals for the duration of the forecast horizon.

All roads lead to the Fed trying to prove themselves again in September. We know how they will act, or not act, when times get better, what will they do if things get worse…. They will have to answer that question, or at least try.

Can the Fed keep getting this chart to bull steepen?

Can we have a “beautiful” recovery?

This is a bit of a play on Mohamed El-Erian’s/Ray Dalio's “beautiful deleveraging” concept from a few years ago.

One of the more interesting under the radar aspects of this years Symposium was, Kristin Forbes of MIT and ex BoE, as chair of the second day conversations, had one overlapping question for all her panels: what is the hypothetical policy response to a right tail outcome in 2021? Let’s say there is an effective and widely distributed vaccine in Q1 2021, pent up demand is met with the combination of supply shocks and pricing power, how does policy respond? What if fiscal support has changed the calculus for hysteresis in the next cycle? As one could have guessed, there was no answer. Governor Bailey of the BoE basically laughed it off. The reason being, policy makers are assuming a post GFC recovery of low NGDP for their entire forecast horizon. And despite a substantial rally in headline risk assets, the market generally agrees.

The market seems to be entertaining a pretty striking inconsistency. One that I think is captured by the relative divergence between the weakness in the dollar and cyclical beta. The market is seemingly having no problem entertaining an 85 or 80 DXY world, but rates will stay where they are forever, tech will outperform everything and NGDP is still dead. Given all the body of work on how big of a multiplier the $ is on the global economic cycle, surely this can’t be. In fact, as the chart below shows, neutral interest rates and the dollar have had a pretty strong relationship going back to the GFC. The dollar can open up new economic outcomes given its strong multiplier effects such as credit, invoicing etc.

G4 avg r* LW model (inv) v USD REER pre Covid

So far, the market has traded the very positive dynamic that the dollar is a “solved problem”, i.e. its skew is no longer violently higher. However, what if the dollar was to really fall 2017 style in rate of change terms, that's a game changer for the global economy and changes the growth/inflation dynamic going forward. 10y breakevens will not be 1.80 in an 80 DXY world.

The big question now is, will the market transition from removing left tail risk premium to pricing in right tail outcomes in terms of growth and inflation? Was this just a mean reversion in terms of left tails leaving the distribution, deflation, Euro fragmentation risk etc. or, is the market beginning to entertain a new regime of fiscal permanence and a faster global economic recovery? In theory we could define the move in breakevens as simply mean reversion. Take what’s priced in caps/floors on inflation swaps, the composition of the move is in that inflation will *certainly be above 1%, but very little of the move is in the possibility that inflation will be significantly above 2%.

With this in mind, we enter three possible camps for the market and inflation right now:

1) The current camp, deflation is off the table, but this will still be a slow recovery, so ED strip stays flat like the dots. Risk assets get benefit of mean reverting data and zero discount rates forever. In that world, duration acts as a vacuum for equity risk premium and the long tech v everything else trade continues to work despite technical hiccups.

2) The second potential camp, fiscal inaction leads markets to at least challenge the idea of a fiscal put and successful policy handoff from monetary. As Coeure always warned us, fiscal lacks "agility." Shorter term liquidity concerns turn into longer term solvency ones again and risk premium shoots up. This risk has been largely put down in places like Europe, as Germany has extended their furlough scheme until the end of 2021. However, it’s hard to say in the US it is off the table.

3) The third camp, the new world of fiscal is here. Aggressive fiscal policy leads markets down a much swifter recovery path, and we begin to question what if neutral rates won’t be 0 forever. This is the world where fiscal transitions from an economic backstop to an economic accelerant. This world is becoming easier to imagine. It is perfectly in the realm of possibilities that the US has an effective and widely available vaccine in Q1 2021 into a new democratic mandate that passes a +$3T HEROs bill.

The market seems to be entertaining a pretty striking inconsistency. One that I think is captured by the relative divergence between the weakness in the dollar and cyclical beta. The market is seemingly having no problem entertaining an 85 or 80 DXY world, but rates will stay where they are forever, tech will outperform everything and NGDP is still dead. Given all the body of work on how big of a multiplier the $ is on the global economic cycle, surely this can’t be. In fact, as the chart below shows, neutral interest rates and the dollar have had a pretty strong relationship going back to the GFC. The dollar can open up new economic outcomes given its strong multiplier effects such as credit, invoicing etc.

G4 avg r* LW model (inv) v USD REER pre Covid

So far, the market has traded the very positive dynamic that the dollar is a “solved problem”, i.e. its skew is no longer violently higher. However, what if the dollar was to really fall 2017 style in rate of change terms, that's a game changer for the global economy and changes the growth/inflation dynamic going forward. 10y breakevens will not be 1.80 in an 80 DXY world.

The big question now is, will the market transition from removing left tail risk premium to pricing in right tail outcomes in terms of growth and inflation? Was this just a mean reversion in terms of left tails leaving the distribution, deflation, Euro fragmentation risk etc. or, is the market beginning to entertain a new regime of fiscal permanence and a faster global economic recovery? In theory we could define the move in breakevens as simply mean reversion. Take what’s priced in caps/floors on inflation swaps, the composition of the move is in that inflation will *certainly be above 1%, but very little of the move is in the possibility that inflation will be significantly above 2%.

With this in mind, we enter three possible camps for the market and inflation right now:

1) The current camp, deflation is off the table, but this will still be a slow recovery, so ED strip stays flat like the dots. Risk assets get benefit of mean reverting data and zero discount rates forever. In that world, duration acts as a vacuum for equity risk premium and the long tech v everything else trade continues to work despite technical hiccups.

2) The second potential camp, fiscal inaction leads markets to at least challenge the idea of a fiscal put and successful policy handoff from monetary. As Coeure always warned us, fiscal lacks "agility." Shorter term liquidity concerns turn into longer term solvency ones again and risk premium shoots up. This risk has been largely put down in places like Europe, as Germany has extended their furlough scheme until the end of 2021. However, it’s hard to say in the US it is off the table.

3) The third camp, the new world of fiscal is here. Aggressive fiscal policy leads markets down a much swifter recovery path, and we begin to question what if neutral rates won’t be 0 forever. This is the world where fiscal transitions from an economic backstop to an economic accelerant. This world is becoming easier to imagine. It is perfectly in the realm of possibilities that the US has an effective and widely available vaccine in Q1 2021 into a new democratic mandate that passes a +$3T HEROs bill.

It is very possible that both tails are underpriced at the moment. The market is fully priced under the assumption that fiscal/monetary will be big enough to to cap any downside risks but not too big to create inflationary pressures. While that is the most likely outcome, it is a very tight distribution for a policy set that we really don't know much about.

Copper may be evidence of the third camp is gaining steam

Does the market have the USDJPY question wrong?

One of the emerging questions in global macro these days is when does USDJPY breakdown and follow the broad dollar index lower. So far, USDJPY has been in a tight range due to very loose funding markets on the one hand and real money flows capping Yen strength on the other. And Yen is not going to trade on relative real rates. The question is, when does this tight range break and do we get this sort of inverse Abenomics move where USDJPY goes back to the 80s?

It's possible the market is asking the wrong question. The right question may be, what if USDJPY is able to absorb these weak dollar pressures and stay above 100, maybe even in this tight 105 range? Let’s say in a world of reflation, rising asset prices and flat term structures, Japanese policymakers are able to get what they want and effectively pin the Yen. That world is a very interesting world for Japanese stocks which are close to pressing up against multiyear resistance.

Nikkei 24k is a huge level if we get there. 3y daily chart.

This may not be actionable right now, but it is something worth watching. Of course, it is too soon to say that USDJPY won’t follow this dollar move lower and that will pose a challenge to Japanese equities, especially in a relative sense. However, given the asymmetry, it is likely worth asking the question of, let’s say we are in a durable reflation and the BoJ has figured out a way to peg JPY, that is about as constructive as it gets for Japanese equities in zero rate world. All of this is happening at close to very interesting technical levels.

Keep an eye on the ECB this week

It was a bit surprising to hear comments from Phillip Lane last week re the current level of EURUSD. It wasn’t anything drastic, and the blog posts from Schnabel have not been particularly worried re the level of the exchange rate.

“At the moment I am not worrying too much about exchange rate developments.”

However, nothing is by accident with Lane, and he wanted it out there that the EURUSD rate matters and the ECB is watching it.

This sets up two questions:

1) Lets for a second entertain the idea that +1.20 worries the ECB. This is something I am not convinced of as the ECB knows the combination of fiscal and the nature of the shock have changed the pass through dynamics. However, in this hypothetical, they care. What do they do? The street is expecting an upsized PEPP, and that makes sense. In theory, QE is two birds with one stone for the ECB, it decreases fragmentation risk and lowers the XR (exchange rate). The problem is, in practice it won’t weaken XR and I think the ECB is well aware of that. The traditional portfolio balance channel ala 2014 is broken. Upsizing PEPP has a much bigger impact on left tail pricing/accommodating fiscal than it does on the portfolio balance channel, so QE in Europe could actually be XR positive…..

Marginal QE effects have changed since Draghi started PSPP

2) Is Lagarde going to entertain rate cuts? This is something that should be off the table, and it likely won't happen because it EURUSD 1.20 is an overrated risk for EA inflation. However, it would be very interesting if Lagarde makes a nudge at getting negative term premium to go a bit further. I.e. testing that lever and see what it does to EUR. And of course, because of that most recent inflation print, she has every right to do so. The knock on if the ECB starts to push the market a bit on getting serious re DFR cuts would be huge. This would open up the same problems of 2019, where the ECB via pushing the dollar higher ends up being a duration vacuum and broadly negative risk. Also, in a more structural sense, it threatens this new world of ELB + fiscal which has been $ negative. It is a much more positive risk FX environment when the only CB really entertaining cuts is NZD and we push the policy handoff narrative. ECB entertaining cuts would threaten that so it is worth watching even if it’s a small probability. As noted above, the $ is the key outlet for a global recovery and the ECB should not want to get in the way of that.

@jturek18